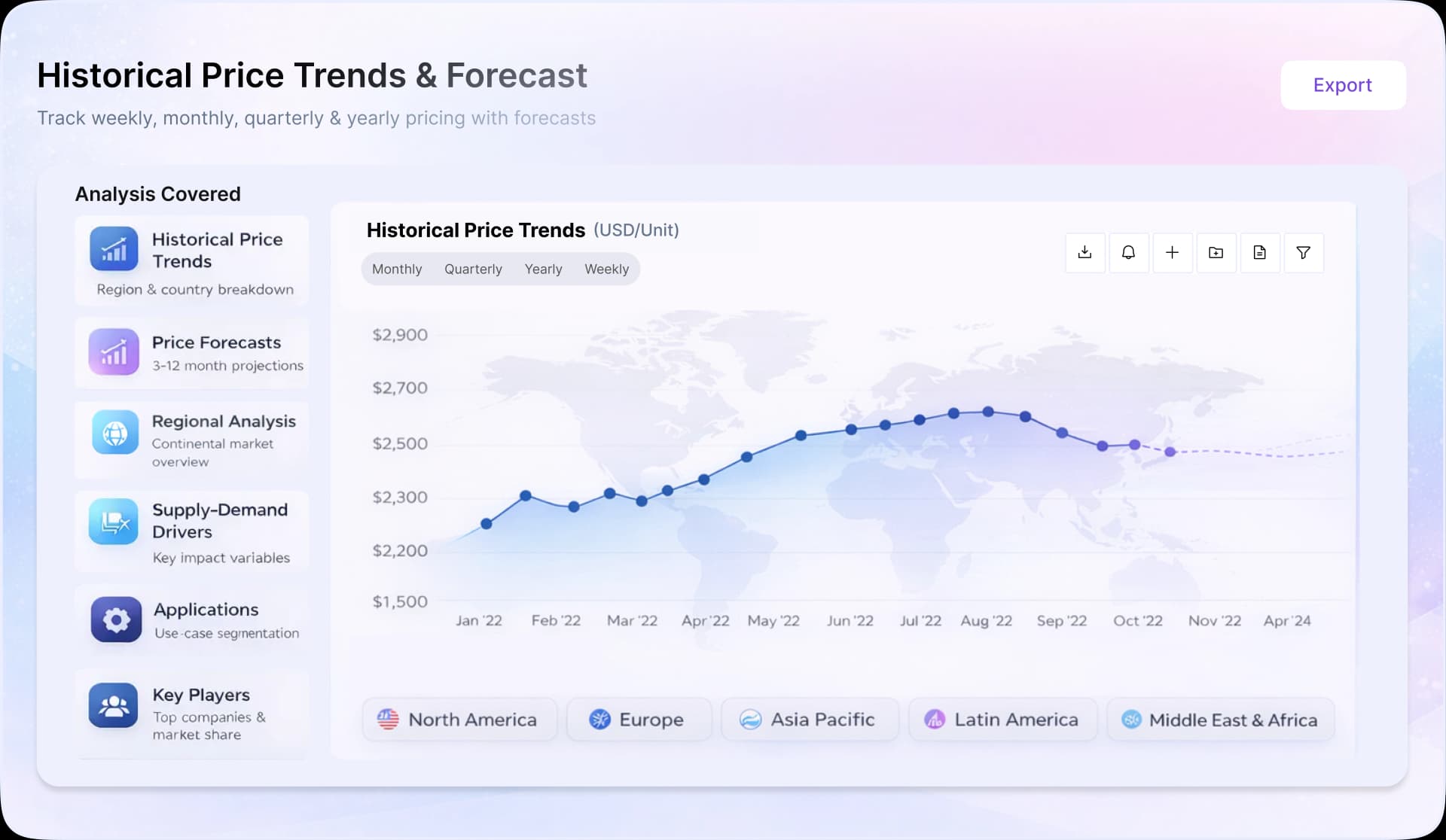

Aluminium Price Trend Analysis 2026: Market Insights, Historical Prices, Latest News, Supply Demand Analysis & Price Drivers

Aluminium Price Trend Q1 2026

| Product | Region | Incoterm Basis | Price | Last Updated Month |

|---|---|---|---|---|

| Aluminium | China | FOB | USD 3,523.91/MT | April 2026 |

| Aluminium | India | CIF | USD 3,573.91/MT | April 2026 |

| Aluminium | USA | CIF | USD 3,610.91/MT | April 2026 |

| Aluminium | Germany | CIF | USD 3,644.91/MT | April 2026 |

| Aluminium | Australia | CIF | USD 3,561.91/MT | April 2026 |

| Aluminium | China | FOB | USD 3,533.10/MT | March 2026 |

| Aluminium | India | CIF | USD 3,588.10/MT | March 2026 |

| Aluminium | USA | CIF | USD 3,620.10/MT | March 2026 |

| Aluminium | Germany | CIF | USD 3,615.10/MT | March 2026 |

| Aluminium | Australia | CIF | USD 3,577.10/MT | March 2026 |

Stay updated with the latest Aluminium prices, historical data, and tailored regional analysis

- Aluminium prices showed a firm global trend in Q1’26, supported by supply disruption fears, low inventories, and constrained global output growth.

- Supply remained tight due to production caps in China, overseas smelter disruptions, and rising concern over alumina and bauxite flows through the Strait of Hormuz.

- Downstream demand stayed healthy in new energy, photovoltaics, energy storage, and infrastructure, while cost pass-through remained uneven in traditional sectors.

Asia

In Asia, aluminium prices moved higher as structural supply tightness and geopolitical risk supported the market. In China, prices were about ~RMB 24.70/kg (Contract FD) in January and around ~RMB 25.70/kg in March, rising by about 4.02%. The increase was driven by the domestic production capacity ceiling, low inventories, and strong demand from new energy vehicles, photovoltaics, energy storage, and computing-related applications. Market sentiment strengthened further in March as the Iran conflict raised concern over shipments through the Strait of Hormuz, a key route for Middle Eastern aluminium exports and raw material imports. Russia’s Rusal plans to redirect aluminium exports from China to Japan and other Asian markets as the Iran conflict disrupted Gulf supplies and drove regional premiums sharply higher. Chinese buyers resisted elevated pricing benchmarks, prompting trade flow shifts amid abundant domestic supply and weakened demand in China. The region accounts for about 9% of global aluminium production capacity, while nearly 23% of global primary aluminium supply comes from the Gulf region. In India, prices were about ~INR 297.91/kg (Contract FD) in January and around ~INR 310.59/kg in March, up by about 4.36%. The rise reflected the same global supply-risk sentiment and firm regional demand conditions.

Europe

In Europe, aluminium prices remained firm because buyers faced higher supply risk premiums after the Iran conflict and the Strait of Hormuz blockade. The market was affected by concern over reduced Gulf supply, possible delays in raw material inflows, and tighter global availability. Low international inventories and stronger LME performance supported European sentiment, while downstream buying remained linked to industrial demand and energy-sensitive sectors. Elevated freight and war-risk costs also kept replacement values high.

North America

In North America, aluminium prices stayed supported by tighter global availability and stronger overseas premiums. Heightened supply concerns in the Gulf region lifted international market sentiment, while the U.S. market also reflected concern over shortages, with Midwest premiums reaching record highs during the conflict period. Even though the region was less directly exposed to Gulf primary metal flows than Europe, global tightness and low inventories kept the market firm.

Analyst Insight

According to Procurement Resource, in the near term, aluminium prices are likely to remain firm with volatility tied to developments in the Strait of Hormuz. Any prolonged disruption to Gulf metal or raw material flows may keep upward pressure on global prices.

Related Report

Our Clients

Procurement Resource Database

Turn price intelligence into action with the Procurement Resource Database. Log in or subscribe to unlock live price trends, historical charts, supplier databases, cost curves, and analyst-backed insights across chemicals, agriculture, energy, packaging, and more. Use these tools to benchmark your contracts, plan budgets with confidence, and stay ahead of market moves on every product you buy.

Aluminium Dashboard Inclusions

0

+Products

0

+Regions

0

+Subscriptions

| Product | Category | Region | Price | Last Updated Month |

| Aluminium | Energy, Metals and Minerals | China | 2943 USD/MT | October 2025 |

| Aluminium | Energy, Metals and Minerals | China | 3106 USD/MT | December 2025 |

| Aluminium | Energy, Metals and Minerals | India | 2989 USD/MT | October 2025 |

| Aluminium | Energy, Metals and Minerals | India | 3163 USD/MT | December 2025 |

Asia

The Chinese aluminium market experienced progressive strengthening through majority of the fourth quarter, reflecting tightening supply conditions and steady downstream consumption. The prices were about 2943 USD/MT (Contract FD) in October and around 3106 USD/MT in December. Alumina availability remained a critical factor supporting production costs, while energy pricing pressures persisted as electricity costs continued to impact smelting economics. Demand from electric vehicles, renewable energy infrastructure, and construction sectors maintained consistent consumption patterns, while social inventory levels declined progressively. By late quarter, accelerated upward momentum emerged as supply-demand fundamentals tightened further, with China approaching its production capacity ceiling.

Indian markets displayed initial stability before entering appreciation during the latter portion. The prices were about 2989 USD/MT (Contract FD) in October and around 3163 USD/MT in December. Domestic supply constraints intensified as import restrictions and stringent quality standards limited material inflows. The production-consumption gap widened as output remained insufficient to meet growing industrial requirements from automotive, infrastructure, and power sectors. Regional premiums expanded significantly above international benchmarks, reflecting transportation costs and limited recycled aluminium availability, with sharp price increases emerging as buyers competed for limited supply.

Europe

European aluminium markets experienced measured appreciation influenced by energy cost dynamics and supply chain adjustments. High electricity prices continued pressuring smelter economics, with some facilities evaluating operational viability under sustained cost burdens. Trade flow realignments following North American tariff implementations redirected Canadian exports toward European markets, partially offsetting domestic production constraints. Demand from automotive and construction sectors remained moderate amid broader economic uncertainties, though consumption proved sufficient to absorb redirected supply volumes. Production curtailments at energy-intensive facilities continued as elevated power costs eroded margins, contributing to tighter regional supply conditions.

North America

North American markets remained under pronounced supply tightness throughout the quarter, experiencing ongoing impacts from tariff policies implemented earlier in the year. Elevated import duties continued creating sustained inventory pressures and elevated regional premiums, with Midwest premiums remaining at heightened levels as domestic production remained insufficient to fully replace reduced import volumes. The effects of previous Canadian import reductions persisted, though late-quarter developments suggested potential trade flow adjustments as persistent inventory depletion made tariff-inclusive imports economically viable again.

| Product | Category | Region | Price | Last Updated Month |

| Aluminium | Energy, Metals and Minerals | China | 2892 USD/MT | July 2025 |

| Aluminium | Energy, Metals and Minerals | China | 2891 USD/MT | September 2025 |

| Aluminium | Energy, Metals and Minerals | India | 2932 USD/MT | July 2025 |

| Aluminium | Energy, Metals and Minerals | India | 2913 USD/MT | September 2025 |

Stay updated with the latest Aluminium prices, historical data, and tailored regional analysis

Asia

Aluminium prices in China fluctuated within a narrow range throughout the third quarter of 2025, reflecting balanced market fundamentals. The average prices were about 2892 USD/MT (Contract FD) in July and around 2891 USD/MT in September. The quarter opened with a brief dip as capacity adjustments and slower downstream orders weighed on sentiment. However, production gradually increased as replacement projects in Yunnan came online, restoring supply stability. Alumina oversupply continued to keep raw material costs contained, supporting smelter margins and encouraging higher output. Demand from power cable, automotive sheet, and foil producers showed mild improvement as companies began restocking ahead of the traditional consumption season. Still, weak off-season activity in the construction and photovoltaic sectors limited stronger gains. Overall, market activity was steady, and aluminium prices held firm amid controlled supply and stable input costs.

In India, aluminium prices showed a fluctuating trajectory with a downward bias during the quarter. Initially, the aluminium price curve moved downward amid the subdued demand and slowdown in metal markets. However, later in the quarter, the market saw renewed strength supported by steady domestic demand and firm industrial consumption. Infrastructure development and power sector expansion provided consistent offtake, while restocking by downstream manufacturers ahead of the festive and construction season boosted short-term procurement. The average prices were about 2932 USD/MT (Contract FD) in July and around 2913 USD/MT in September.

Europe

European aluminium markets recorded moderate price gains over the quarter, primarily driven by limited regional supply and firm industrial activity. Sanctions on Russian metal and persistent high energy costs curtailed output from several smelters. Imports from North Africa and the Middle East helped offset domestic shortages, yet availability remained tight. Demand held steady across transportation, renewable energy, and defence manufacturing, while construction activity stayed subdued due to financing constraints and slower project execution. Despite modest demand growth, supply-side challenges sustained a firmer price trend through the period.

North America

Aluminium prices in North America rose gradually during Q3 2025, influenced by tariff-related cost pressures and steady infrastructure demand. The extension of Section 232 tariffs increased input costs, prompting shifts in sourcing strategies toward regional and allied suppliers. Domestic production levels remained stable but faced high energy costs and intermittent supply chain disruptions. End-use industries, particularly automotive and construction, maintained consistent procurement, reinforcing a steady consumption base. Trade activity strengthened toward the end of the quarter as buyers secured inventory ahead of anticipated seasonal demand.

| Product | Category | Region | Price | Last Updated Month |

| Aluminium | Energy, Metals and Minerals | India | 2753 USD/MT | April 2025 |

| Aluminium | Energy, Metals and Minerals | India | 2843 USD/MT | June 2025 |

| Aluminium | Energy, Metals and Minerals | China | 2743 USD/MT | April 2025 |

| Aluminium | Energy, Metals and Minerals | China | 2857 USD/MT | June 2025 |

Stay updated with the latest Aluminium prices, historical data, and tailored regional analysis

Asia

In the India subcontinent, aluminium price trend witnessed a fluctuating trajectory with a slight upwards bias in Q2 of 2025. The prices were about 2753 USD/MT (Contract FD) in April and around 2843 USD/MT in June. Following some volatility at the start of the quarter, the market evidenced resilience, fueled by constricting supply in combination with relatively stable demand. The sudden dip observed was mainly due to a mix of external economic factors, including global tariff impositions, and regional shifts in consumption patterns. Despite the fluctuations, prices remained on an overall upward slope toward the end of the quarter.

Meanwhile, Chinese markets also witnessed similar price movements on the aluminium price curve. The dip witnessed earlier in the quarter was due to the same tariff impacts on international trade and domestic supply chain disruptions. Consequently, China recovered comparatively quickly, with prices tending to rise gradually as the quarter progressed. The prices were about 2743 USD/MT (Contract FD) in April and around 2857 USD/MT in June. Domestic consumption within China was strong, especially in the industrial and infrastructure spaces, which eased the downward pressures. The resumption of an uptrend in June was indicative of increasing confidence from the downstream sector, though the external pressures from the US tariffs remained a major challenge.

Europe

Aluminium price graph in Europe were influenced by macroeconomic trends and tensions between trade. The market opened Q2 with a comparably muted price range, characterized by uncertainty at the external level, such as persisting trade tensions between major economies. However, despite these pressures, the European market saw a gradual increase in aluminium prices, with some fluctuations along the way. One key factor contributing to this trend was the region's struggle with energy costs, particularly in countries heavily reliant on energy-intensive aluminium production. The slight recovery in prices towards the end of the quarter can be seen as a response to better demand conditions, particularly from sectors such as automotive and construction.

North America

The North American market for aluminium during Q2 in 2025 exhibited volatility, which was mainly the result of ongoing tariff uncertainties. First, aluminium prices in the US trended slightly lower as the market responded to the prevailing trade uncertainty. he US government’s tariff policies, including the imposition of additional tariffs on imports, had a chilling effect on international aluminium supply. However, later in the quarter, there was a uptick in prices, fueled by supply chain adjustments and a more optimistic domestic demand. The recovery of the region was also supported by continued efforts to sustain domestic production levels in spite of the external pressures.

| Product | Category | Region | Price | Last Updated Month |

| Aluminium | Energy, Metals and Minerals | China | 2737 USD/MT | January 2025 |

| Aluminium | Energy, Metals and Minerals | China | 2859 USD/MT | March 2025 |

| Aluminium | Energy, Metals and Minerals | India | 2874 USD/MT | January 2025 |

| Aluminium | Energy, Metals and Minerals | India | 3002 USD/MT | March 2025 |

Stay updated with the latest Aluminium prices, historical data, and tailored regional analysis

Asia

During the first quarter of 2025, Chinese aluminium prices experienced a consistent upward trend. The prices were about 2737 USD/MT (Contract FD) in January and around 2859 USD/MT in March 2025. This rise was primarily fueled by sustained demand from the major downstream sectors, such as automotive and construction. Yet, the main cause behind this growth was the supply shortage in the region. Since raw material supply experienced minor interruptions, the Chinese aluminium market responded with gradual price hikes. These were added to by continuous global trade policy adjustments, which triggered some volatility in the market sentiment. While there were uncertainties in the external trade environment, the demand was still firm, especially with China's substantial dependence on aluminium for developing infrastructure.

India's aluminium market also trended similarly to China with a moderate upsurge in prices during Q1’25. The prices were about 2874 USD/MT (Contract FD) in January and around 3002 USD/MT in March. The price increase was mostly backed by a stable demand in the construction and vehicle sectors, both of which contribute towards aluminium consumption in the nation. Moreover, supply disruptions and logistics issues caused some price volatility, adding to the overall upward trend. India's aluminium market also reflected the global transition towards more sustainable industrial processes, which ensured consistent demand for the commodity, particularly within the renewable energy industry.

Europe

In Europe, the market for aluminium experienced divergent trends during the initial quarter of 2025. Prices were affected by both regulatory risks and rebounding demand from markets like electric vehicles (EV) and solar. The announced prohibition on Russian aluminium imports and reduction in stocks on the supply side supported the rise in the prices. Amidst these issues, automotive and industrial sector demand did not lessen. By quarter-end, prices remained weakly stabilized but were still subject to continued regulatory and supply issues.

North America

North America witnessed uniform price appreciation of aluminium during the first quarter of 2025. Prices surged due to a combination of strong automotive sector demand and tight raw material supplies. Market players had to deal with high alumina costs, adding to production costs. The aluminium ingot industry was robust, supported by the demand from the automotive industry and declining warehouse stocks. Owing to fear of changing tariffs and trade policies, the North American aluminium industry stayed firm, with prices climbing further as a result of constant demand.

| Product | Category | Region | Price | Last Updated Month |

| Aluminium | Energy, Metals and Minerals | China | 2933 USD/MT | October’24 |

| Aluminium | Energy, Metals and Minerals | China | 2769 USD/MT | December’24 |

| Aluminium | Energy, Metals and Minerals | India | 2856 USD/MT | October’24 |

| Aluminium | Energy, Metals and Minerals | India | 2872 USD/MT | December’24 |

Stay updated with the latest Aluminium prices, historical data, and tailored regional analysis

Asia

The fourth quarter of 2024 saw Aluminium prices in Asia following a mixed trajectory. China, the world's largest producer, experienced a notable downturn in December after reaching peak levels in early November. The East China market witnessed weakness, primarily driven by lower-than-expected downstream demand and resistance to high-priced raw materials. The monthly average contract FD prices in the Chinese market went from about 2933 USD/MT in October’24 to around 2769 USD/MT in December’24.

The market dynamics were further complicated by China's significant policy shift to end tax rebates on semi-manufactured Aluminium exports from December 1, which initially created market uncertainty. Inventory levels in China showed positive movement, with social inventory decreasing by 80,000 tons through December, indicating healthy destocking activity despite price pressures. On the other hand, the price trajectory was mostly stable in the Indian aluminium market, as the monthly average contract FD prices went from about 2856 USD/MT to around 2872 USD/MT from October’24 to December’24.

Europe

European Aluminium markets demonstrated resilience in Q4’24, despite ongoing regional challenges. The quarter began with strong momentum, particularly benefiting from the EU's decision to impose tariffs on Chinese electric vehicles, which indirectly supported regional Aluminium demand. European smelters, which had previously faced production cuts due to energy constraints following the Ukraine conflict, showed signs of recovery. The London Metal Exchange (LME) prices reflected this renewed confidence, reaching five-month highs in November. However, the market moderated towards the end of the quarter as global supply concerns, particularly regarding Guinean bauxite exports, influenced trading patterns.

North America

The North American Aluminium market in Q4’24 was characterized by cautious trading amid complex global dynamics. The market responded to international supply shifts, particularly following China's export policy changes. Trade tensions and tariff discussions continued to influence market sentiment, while strong demand from the automotive and renewable energy sectors provided underlying support. The region's prices largely followed global trends, with some premium over other markets due to logistics costs and regional supply-demand dynamics.

Asia

The price of aluminium remained volatile in the Chinese market during the third quarter of 2024. The price trajectory exhibited fluctuations, with notable ups and downs. At the start of the quarter, prices continued the declining trend from the previous quarter, driven primarily by the higher production of aluminum in July. A significant increase in aluminum ingot production during this month boosted supply and contributed to the price drop. On the demand side, the downstream aluminum processing industry operated at a subdued pace, with downstream enterprises running at low capacities due to a notable decline in orders.

This downward trend persisted for some time, and by the end of the month, aluminum prices had fallen close to their marginal cost. In August, the market saw a slight recovery, driven by low inventory, although demand remained average. This cautious market sentiment was influenced by expectations of interest rate cuts from the U.S. Federal Reserve, which were confirmed in late September. Following this announcement, aluminum prices began to rise.

Europe

The price of aluminum fluctuated during the given quarter. At the beginning of the period, market conditions were weak, as demand from downstream sectors such as construction, automotive, and others was low. In Germany, the aluminum market was slowing down, with limited availability of recycled materials. Similarly, Italy and Spain saw subdued demand for secondary aluminum. Competition for aluminum scrap was high, which led to reduced profit margins and challenges for smaller yards.

Although demand remained low for most of the quarter, tighter supply conditions provided some support to the aluminum market. Availability was significantly restricted due to low production levels resulting from substantial cuts in the past two years, a reduction in Russian metal supply caused by self-sanctioning by consumers, and official sanctions from the U.K. and U.S. governments. The market saw an improvement, with prices rising following the announcement of U.S. federal cuts, which boosted market sentiment.

North America

In North America, aluminum prices were expected to benefit from the anticipated interest rate cuts by the U.S. Federal Reserve. When the Fed announced a 50-basis point reduction, aluminum prices rose. The increase was driven by a weaker U.S. dollar, which made aluminum more affordable for international buyers using other currencies. This rise contributed to higher aluminum prices both domestically and globally.

| Product | Category | Region | Price | Last Updated Month |

| Aluminium | Energy, Metals and Minerals | China | 2893 USD/MT | Q2 2024 |

Stay updated with the latest Aluminium prices, historical data, and tailored regional analysis

Asia

In the early phase of Q2’24, the aluminium prices in China were driven by the surge in raw material prices and limited supply of the commodity in the region due to a constrained influx of overseas imports and the slow recovery of the market post-holiday season. The supply disruptions were further elevated by a halt in operations at Rio Tinto’s Australian unit. However, as June approached, the pace of the market slowed down, with the downstream sectors like photovoltaic modules presenting a dim demand for the commodity.

In a similar phase, Yunnan aluminium enterprises increased their production capacities, adding additional pressure on the trading sector and widening the supply-demand gap. With the quarter approaching its end, the market moved towards a more stable trend, and traders closed the market at a price quotation of a monthly average of 2893 USD/MT, with a small gain from approximately 2796 USD/MT in the initial phase.

Europe

In the second quarter of 2024, the European aluminium market faced significant challenges, particularly in Germany. Despite efforts to boost recycled aluminium production, which reached 685,000 tons from January to March, semi-finished aluminium production saw a notable decline, with an overall reduction of 6%.

Rolled aluminium products experienced a moderate 5% decline, while extruded products dropped by 13%, influenced by competitive pressures from Turkish imports. High energy costs and a sluggish economic environment exacerbated the situation, with demand from critical sectors like construction and electric vehicles remaining low.

The competitive landscape was further strained by Turkish manufacturers benefiting from cheaper Russian primary metal, raising concerns about unfair trade practices. Despite cautious optimism from Aluminium Deutschland, citing slight increases in tube and aerosol can deliveries, the industry remains wary of high energy costs, potential economic recession, and regulatory challenges. This environment has led to a subdued outlook for aluminium prices in Europe, with market conditions reflecting both reduced production capacities and competitive international pressures.

North America

In the second quarter of 2024, the Biden government announced additional tariffs on the imports of aluminium from mainland China ahead of the election season in order to protect its domestic market from cheap Asian imports. Although the interest of the US market in Chinese imports had already declined significantly since the advent of the new year, these tariffs have made the situation more complex.

The tensions in the market become more significant as the aluminium markets are already strained by sanctions on Russian trade. The immediate of these tariffs was quite visible in the prices of aluminium and its derivatives which soared around the middle of the quarter. However, as domestic production geared up to cater to the in-house demand, the prices of the commodity eventually trailed off.

| Product | Category | Region | Price | Last Updated Month |

| Aluminium | Energy, Metals and Minerals | Europe | 2343.02 USD/MT | March 2024 |

| Aluminium | Energy, Metals and Minerals | China | 2672.42 USD/MT | March 2024 |

| Aluminium | Energy, Metals and Minerals | India | 2473.02 USD/MT | March 2024 |

Stay updated with the latest Aluminium prices, historical data, and tailored regional analysis

Asia

In the first quarter of 2024, aluminium prices in China encountered significant fluctuations driven by the complex interplay of supply constraints, demand dynamics, and macroeconomic factors. Although, starting with a decline in January due to decreased alumina costs and logistical challenges, prices saw a moderate recovery towards the end of the quarter. The severe weather conditions and logistical disruptions in bauxite supply initially tightened the market, but improved production volumes gradually alleviated these constraints.

Despite low inventory levels providing some price support, the seasonal low consumption period and the Spring Festival holiday led to reduced orders and a potential inventory build-up. By February, aluminium prices stabilized as downstream industries resumed operations post-holiday, supported by steady demand from the automotive and construction sectors.

In March, the prices saw further price strengthening, influenced by the Federal Reserve's anticipated interest rate cuts, improved downstream consumption, and partial resumption of production in Yunnan. Overall, the quarter ended with aluminium prices in a moderately strong position, reflecting a balance of supply-side challenges and recovering demand.

Europe

In the first quarter of 2024, the European aluminium market, particularly in Germany, faced significant production declines across nearly all subsectors, escalating the pressure from increasing imports and creating a challenging environment for domestic manufacturers. Recycled aluminium production, crucial for Europe's decarbonization goals, fell sharply, with Germany producing 685,000 tonnes, marking a notable decrease. This downturn was further compounded by growing competitive pressure from countries like Turkey, whose market share in Germany's aluminium extrusion sector has increased significantly.

Despite these challenges, there is optimism for future demand growth in aluminium extrusions, driven by a post-pandemic resurgence and increased market interest. However, the current position of the market highlights the need for strategic responses to competitive pressures and supply chain disruptions to stabilize and potentially reverse the declining production trends in the European aluminium industry.

North America

The North American aluminium market registered moderate gains in the second quarter of 2024. The pricing trajectory of the commodity was influenced by the changing outlook of the global trading sector amid the ongoing geopolitical tensions and disruption of traditional routes. This led to constriction of supply chains and, therefore, limited the influx of the commodity in the region. Although, demand for aluminium grew gradually, outpacing domestic production as well as overseas import, widening the supply-demand gap. Meanwhile, global mining activities in key countries also took a downturn amid the increasing environmental regulations, further constricting the supply chains and asserting positive pressure on aluminium prices.

Asia

The aluminium price trend was observed to be constantly fluctuating throughout the second half of the year 2023. In the Asian region, the Chinese market was relatively more stable and positively inclined than the Indian market. In the Chinese domestic market, the average monthly prices rose by about 4% from July to October, then marginally slid in November, only to rise again in December.

Conclusively the third quarter was more inclined than the fourth. The dwindling nature of prices in the last three months was primarily because of the shipping curtailments in the Red Sea and political, social, and economic unrest in the Middle East.

The average monthly prices (Contract, FD) in China went from about 2546 USD/MT (Contract, FD) in July’23 to around 2643 USD/MT in December’23, registering an overall inclination of about 3%. On the other hand, the Indian aluminium industry witnessed even more fluctuations as the prices here wavered within an even narrower range. The monthly average prices in the Indian market went from around 2440 USD/MT (Contract, FD) in July to about 2443 USD/MT in December.

Europe

The European aluminium market was evidently unstable during the said period. At the beginning of the third quarter, the prices first declined from July to August because of high inventory support and then inclined in the next set of months as the demand increased. As the last quarter approached, the market movement became even more sullen.

Primarily, the sluggishness in the global aluminium market was reflected in the regional price trend; along with that, the strained performance of the downstream construction industry was also playing a major role. Overall, mixed market performance was witnessed.

North America

The American aluminium industry almost replicated the market behavior of its European counterpart as the prices were witnessed to be oscillating here as well. The American market had a slow start in July because of a questionable performance by the construction and infrastructure sectors. However, as the inventories started running out, some temporary and marginal improvement was seen in the prices. However, the latter quarter again turned meek, with a tepid turn in the price graph.

International trade suffered because of the Panama Canal restrictions as the Houthi attacks increased in the Red Sea. The market could not recover from dull demands for the majority of the last quarter. The prices were oscillating at the lower end.

Asia

The Asian Aluminium market exhibited mixed price trend in the first half of 2023. From January to February, prices rose marginally because steady demands from downstream manufacturing sectors supported cost. But in the next month, prices started sliding majorly because the USA imposed a 200% tariff on Russian aluminium imports, which is the second biggest producer of Aluminium in March 2023. This diverted Russian supplies from America to its friendly Asian nations, which reduced upstream cost support, aiding declining trend.

The only jump in the price trend came at the change of quarter because of a sudden influx of international orders because of US tariffs, but soon the oversupply took over, and prices started declining again after April. Aluminium prices started in January at an average of about 2705 USD/MT (Contract FD) in the Chinese domestic market and ended quarter 2 with an average of around 2610 USD/MT (Contract FD) on June 23’. Indian Aluminium market too exhibited similar trend in the said period, with prices averaging at around 2512 USD/MT (Contract FD) in June’23.

Europe

European Aluminium prices also exhibited mixed patterns. Quarter one had a slow start because suppliers made conscious purchases amidst ambiguity around Aluminium prices. Also, struggles with inflation and high energy prices rendered severe cost of living crisis. Germany even underwent an economic recession in February 2023. These events impacted European consumers’ purchasing capacities and behaviour, making it more necessity centric. So, because of dipped downstream demands, price trend for Aluminium remained dull and drowned in quarter one.

But as the second quarter approached, US tariffs on Russian imports created scarcity in Western markets. Moreover, because of some economic rebound, markets started thawing a little, which increased downstream demands, and existing inventories were already limited because of conscious purchases by suppliers and could not support the rising demands. So, the prices were set on an inclined trajectory for most of Quarter 2.

North America

The North American Aluminium market almost replicated the European market for price trend. Quarter one started with saturated inventories as economic setbacks from the collapse of 2 major US banks and increased interest rates negatively impacted the purchasing activities and abbreviated the downstream demands. So, the prices laid low for most of the first quarter.

As the second quarter approached effects of America’s 200% tariff imposition on Russian Aluminium imports started showing an impact. Upstream costs rose as inventories started depleting, catering to the growing demands from downstream manufacturing and construction sectors. So, the Aluminium prices mostly dwelled on the higher side for the majority of the second quarter.

Asia

With the dollar strengthening and the interest rates hike by the central bank the feeling of economic recession dominated the market’s sentiments and as a result, the bulk commodities plunged. The price trend of aluminium fell during the said period showing a slight increment from time to time. Though the production costs stabilized during the third quarter, the overall prices remained weak owing to muted demand from downstream sectors. The prices of aluminium ingots averaged 18453.33 RMB/MT towards the end of the third quarter.

The Chinese government had imposed restrictions on heavy industries with a plan to reduce carbon emissions, which had an impact on aluminium prices. Incessant power shortages in the country also disturbed the supply chain of the commodity this year. Aluminium prices stabilized a bit during the fourth quarter for a short term, however, overall prices kept weak averaging 18716.67 RMB/MT towards the end of December’22.

Europe

The European region faced the direct consequences of the Russia-Ukraine conflict triggering an acute energy crisis. With the high-cost inflation and high operating rates, the manufacturers passed on the higher prices to the consumers to cushion their profits resulting in demand destruction. The lowered demand caused the European manufacturers to seek to offload expensive metal leaving limited buffer stock only. Hence, the price trend for aluminium dwindled in the European domestic market.

North America

The aluminium prices in the US domestic market were in line with the global outlook. The prices fell owing to weak demand from the construction and electrical sectors amid high sourcing and operating costs.

Asia

In China, Aluminium prices reached a six-month low owing to the stringent covid lockdown restrictions amidst the rising cases. The fear in the market because of uncertainty and low running capacities of the industries caused the prices to fall in the domestic market.

However, after relaxing the restrictions, the industries started churning the metal at enhanced capacities, which led to stockpiling in the market because of the muted demands in downstream sectors. Hence, the price trend crashed further, averaging around 2685 USD/MT on the domestic front.

Europe

The production of primary Aluminium is a highly energy intensive process. The European industrial sector is already facing an acute energy crisis due to the ongoing confrontation. The high production costs, complex supply, and increased demand from the automotive industry caused the Aluminium price increase in the region.

With sanctions against Russia, the European governments are frantically working to meet the domestic demands. During this forecast quarter, the prices averaged 2950 USD/MT on London Metal Exchange.

North America

The price trend were in line with its Asian counterpart due to the muted demand and higher production levels. The price of Aluminium averaged 2400 USD/MT (approx.) in the United States.

Asia

In March 2022, in China, per ton price of Aluminium was 22640 RMB/MT. Secondary or recycled Aluminium makes for a sizable portion of worldwide Aluminium usage. Due to its cost-effectiveness, scrap from automobiles, equipment, beverage cans, and machinery was recycled and reused.

Reprocessing secondary metal or trash uses a fraction of the energy necessary to produce new metal from mining, resulting in less environmental damage. In addition, measures such as the creation of automobile disassembly and shredding factories, as well as depollution centres, aided market expansion. Furthermore, widespread usage of the metal in the transportation industry was boosted the Aluminium demand even further.

Europe

Since the beginning of 2022, European aluminium prices have risen by roughly 15%, surpassing its historic high of October 2021 - an increase of more than 60% compared to January 2021. Because energy accounts for a large share of production costs, more than a third, a fast increase in the price of gas has a significant influence on company profitability, particularly in Europe, where natural gas prices have climbed by about 550% from December 2020 to December 2021.

As a result, European aluminium manufacturers are forced to make a difficult decision. Either they shut down their smelters or they cut back on production, even if it means losing money. This is the option selected by Europe's largest smelter at the end of December 2021. Aluminium prices on LME were 3300 USD/MT in January 2022.

Asia

China had begun to reduce its Aluminium production in 2021 and instead chose to import large volumes which not only created a global shortage of the metal but also increased the prices for the commodity. In November 2021, an Aluminium factory in Yunnan, China suffered a major explosion. This led to a complete halt to production in the region, reducing the production capacity by 300,000 tonnes which impacted the already suffering market supply.

Europe

In most European countries, the energy prices had been increasing significantly in the last quarter of 2021 making the metal’s production highly expensive in the region. In Germany, the average EPEX market price was recorded at 220 USD per megawatt hour which had almost doubled from last year. In France, it had been tripled to close to 300 USD per megawatt hour. This surge in energy prices pushed the major smelters to cut down their productions.

The Aluminium Dunkerque in France, a major producer of Aluminium slab and ingots had reduced its production capacity by 3.7% as compared to previous year. Romanian producers, like Alro, also commentated that Aluminium production had been unsustainable in the final quarter of 2021.

North America

In 2021, the US was the largest importer of the metal. Aluminium prices had been soaring high in the final quarter 2934 USD/MT as compared to the 2004 USD/MT in the first quarter of the year. Aluminium prices are likely to increase in the upcoming times owing to the supply shortages, the shift towards greener economy, the reduction of carbon emissions in China and the rising demand from the automotive industry for electric vehicles. The high prices of energy sources are also key growth drivers in this market.

Latin America

In Brazil, Alcoa, a major producer of the metal, declared to resume its plant production activities in Sao Luis, Alumar with a plant capacity of 260,000 tonnes per year to keep up with the changing global scenario for the Aluminium market. The plant is resuming operations in spite of the hydro-electric problems in Brazil owing to the drought. This increase in production and supply of Aluminium is likely to impact the market soon. In the final quarter of 2021, Aluminium prices were 14.64k BRL/MT.

Asia

The production of the metal in China during the first quarter was 6.3 % higher as compared to the previous year. The demand for the metal is being pushed by the shift towards a greener economy and its demand and consumption are expected to go up in the upcoming years.

However, at the same time in China, the carbon emissions were recorded at 420 million tonnes in 2020, which was then capped at 45 million tonnes for 2021 which means that Beijing will witness a change in its supply forms and switch to secondary supply like metal scraps which may generate a market uncertainty.

Other issues are the energy cap imposed on smelters and workers due to the coal shortage. The production plateaued in certain regions which increased the prices along with a growing consumption as more and more people shift towards electric vehicles.

Europe

Due to the supply deficit, the prices had been increasing in Europe. Due to excessive Chinese imports, the supply gap for Aluminium was widened as the market was undersupplied by 480,000 tonnes of the metal and this shortage is likely to continue in the upcoming years, as reported by major financial or manufacturing firms like Alcoa, ING and Dutch Multinational. The energy shift towards renewable sources has been a major growth driver for the Aluminium industry.

North America

The prices witnessed a three-year high in 2021 in the US. Production had been booming in China. The market was tight amidst supply concerns. In the meantime supply concerns were rising with the increasing demand for manufactured goods. Aluminium prices in London Metal Exchange were as high as 2535 USD/MT in the second quarter of 2021. The Chinese imports for the metal had increased by 36% in April 2021, which led to the price flare.

Asia

In the first half of the year, price of the metal China had dropped but started to recover slowly after March. From 2234 USD/MT in the beginning of the year, Aluminium prices plummeted to 1791 USD/MT in March which continued till July, as demands came down due to the shutting down of industries in the first quarter owing to the pandemic.

In July, the price rose again to 2217 USD/MT and dropped to 2188 USD/MT in September. The prices started to rise again in October and surpassed 2500 USD/MT. By December, Aluminium prices in China had reached 2617 USD/MT, the highest in 2020. The Chinese production witnessed record high values at close to 37 million tonnes of production.

Europe

The falling demand for the metal due to the pandemic caused the prices to fall steadily in the first half of 2020. The global economy had slowed down as most industries like automobile, aerospace and construction had been hit critically by the lockdowns which resulted a slump in its global consumption and demand.

The Norwegian Aluminium producer Norsk Hydro reported that the primary global consumption had fallen by 9.41% in the first half of 2020. The production however, at the same time, had been steady with a surplus in the market. Nevertheless, the economies started to expand after the lockdowns were lifted and demand and prices were on the rise in the third and final quarters of 2020.

North America

The average price in the US in 2020 was 1704 USD/MT. The demand had plunged in the first half of 2020 as a result of shutting down of industries due to the COVID-19 pandemic. Economic slowdown and a surplus supply caused the prices to decline further.

The Aluminium LME (London Metal Exchange) prices in the beginning of 2020 were 1772 USD/MT which went down to 1602 USD/MT in the first half of the year. This price slump continued till July. However, Aluminium prices started to recover in August and by October the prices had exceeded 1800 USD/MT. In November, the prices went up to 2000 USD/MT and the highest price in the year, 2051 USD/MT, was recorded in the first week of December. The demand for the metal had risen as production activities resumed all around the world.

Latin America

In Brazil, the prices were affected not just by the pandemic and overproduction, but also by the shutdown of four production lines of Albras due to an electrical fire. In Venezuela, the Aluminium market was crippled due to the absence of a commercial vision, the dropping value of Bolivar exchange rate against USD, infrastructure problems along with political instability in spite of having immense hydroelectric power and modern alumina refinery and bauxite supplies.

About Aluminium

Aluminium or aluminum, as a metal, is derived from Aluminium-containing minerals. Small amounts of Aluminium can be easily found in dissolved water. It is light in weight and silvery-white in appearance. The main ore of Aluminium is bauxite. The metal is highly reactive in nature and finds application in a wide range of industries.

Aluminium Product Detail

Al

Chemicals, Cans, Foils, Kitchen utensils, Window frame, Beer kegs, Aeroplane parts, Electrical transmission lines

7429-90-5, Aluminium, Aluminium Metal, Aluminium Powder

Rio Tinto plc, United Company Rusal Plc, American Elements, PT Timah (Persero) Tbk, Aluminium Corporation of China Limited (CHALCO), Alcoa World Alumina and Chemicals (“AWAC”) (Alumina Ltd)

Regional Coverage

Asia Pacific

Europe

North America

Latin America

Africa

CurrencyUS$ (Data can also be provided in local currency)

Supplier Database AvailabilityYes

Customization ScopeThe report can be customized as per the requirements of the customer

Post-Sale Analyst Support360-degree analyst support after report delivery

Note: Our supplier search experts can assist your procurement teams in compiling and validating a list of suppliers indicating they have products, services, and capabilities that meet your company's needs.

Aluminium Production Process

- Production of Aluminium via Bayer and Hall–Heroult Process

Aluminium's production process is carried out by combining two processes, namely, the Bayer process and the Hall-Heroult process. The bauxite ore is processed into alumina by utilising these two processes and finally, the obtained alumina is converted into Aluminium.

Methodology

The displayed pricing data is derived through weighted average purchase price, including contract and spot transactions at the specified locations unless otherwise stated. The information provided comes from the compilation and processing of commercial data officially reported for each nation (i.e. government agencies, external trade bodies, and industry publications).

Our Price Analysis Methodology

Schedule A Demo

Experience how Procurement Resource transforms raw material price data into clear, decision ready intelligence. Optimise your performance with reliable, expert market data and analysis. Schedule your demo today to experience a live walk-through where our experts will showcase interactive price charts, forecasted prices, and insights driving the prices for your key commodities, tailored to your workflows. Contact us now!

Our Team will be happy to assist you

We are just a text away

Still Need Help ?

Other Related Reports

Aluminium Can Production from Two-Piece or Three-Piece Drawing

This report provides the cost structure of aluminium can by two-piece or three-piece drawing methods.

Aluminum Chloride Production from exothermic reaction

An exothermic reaction between aluminium metal with chlorine or hydrogen chloride yields aluminium chloride at large scale.

Aluminium Sulfate Production from Alum Schists

The report involves the cost analysis of production of aluminium sulfate using alum schists which are mixtures of iron pyrite, aluminium silicate and various bituminous substances.

Subscription Plans

Unlock full access to Procurement Resource's price databases, interactive charts, and short-term forecasts for thousands of commodities. Elevate your sourcing decisions by comparing prices across regions, downloading historical data, and layering in analyst-backed insights, all with our flexible plans that scale as your portfolio grows.

Still have any Questions

Contact Us

Price Trend Dashboard - What's Included

Price trends across a diverse portfolio of categories amd products, spanning board to niche chemicas

Coverage extendable to grade-specific chemicals based on procurement requirements

Regular price tracking supported by robust historical datasets

News, policy updates, and key market drivers impacting price movements

Short-term and long-term price outlooks and forecasts

Supply–demand dynamics and capacity-driven market analysis

- Unlimited Users

- Historical Monthly Price

- USA, Europe, APAC Covered

- Monthly Forecast

- 12 Months validity

- News & Events

- 50 Products (Refer Next Page For List)

Related News

View All

QatarEnergy expands production shutdown to fertilizers polymers and aluminium after attacks disrupt LNG facilities and energy exports

Aluminium Prices Declined Overnight As Supply In China Increased After Production Resumption In Guizhou And Sichuan

Speira Has Decided To Close The Aluminium Smelting Operations At Its Rheinwerk, Germany Facility

Why Procurement Database

Assistance from Experts

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Client's Satisfaction

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Assured Collaboration

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Global Insights

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...