Cocoa Price Trend Analysis 2026: Historical Prices, Price Drivers, Latest News, Market Insights & Supply Demand Analysis

Cocoa Price Trend Q1 2026

| Product | Region | Incoterm Basis | Price | Time Period |

|---|---|---|---|---|

| Cocoa | China | CIF | USD 3217/MT | April 2026 |

| Cocoa | India | FOB | USD 1306/MT | April 2026 |

| Cocoa | USA | CIF | USD 3,397/MT | April 2026 |

| Cocoa | UK | CIF | USD 3,391/MT | April 2026 |

| Cocoa | Canada | CIF | USD 3,400/MT | April 2026 |

| Cocoa | China | CIF | USD 3,061.49/MT | March 2026 |

| Cocoa | India | FOB | USD 1301/MT | March 2026 |

| Cocoa | USA | CIF | USD 3241.49/MT | March 2026 |

| Cocoa | UK | CIF | USD 3245.88/MT | March 2026 |

| Cocoa | Canada | CIF | USD 3244.49/MT | March 2026 |

Stay updated with the latest Cocoa prices, historical data, and tailored regional analysis

- Cocoa prices declined globally in Q1’26 as improved harvest outlooks in West Africa shifted the market from deficit to surplus, reversing the previous upward cycle.

- Feedstock and supply dynamics weakened price support, with favourable weather boosting production while exporters locked in future prices to hedge volatility.

- Downstream demand remained subdued earlier due to high costs and reformulation trends, before showing a slight pickup during the Easter season supported by seasonal consumption patterns.

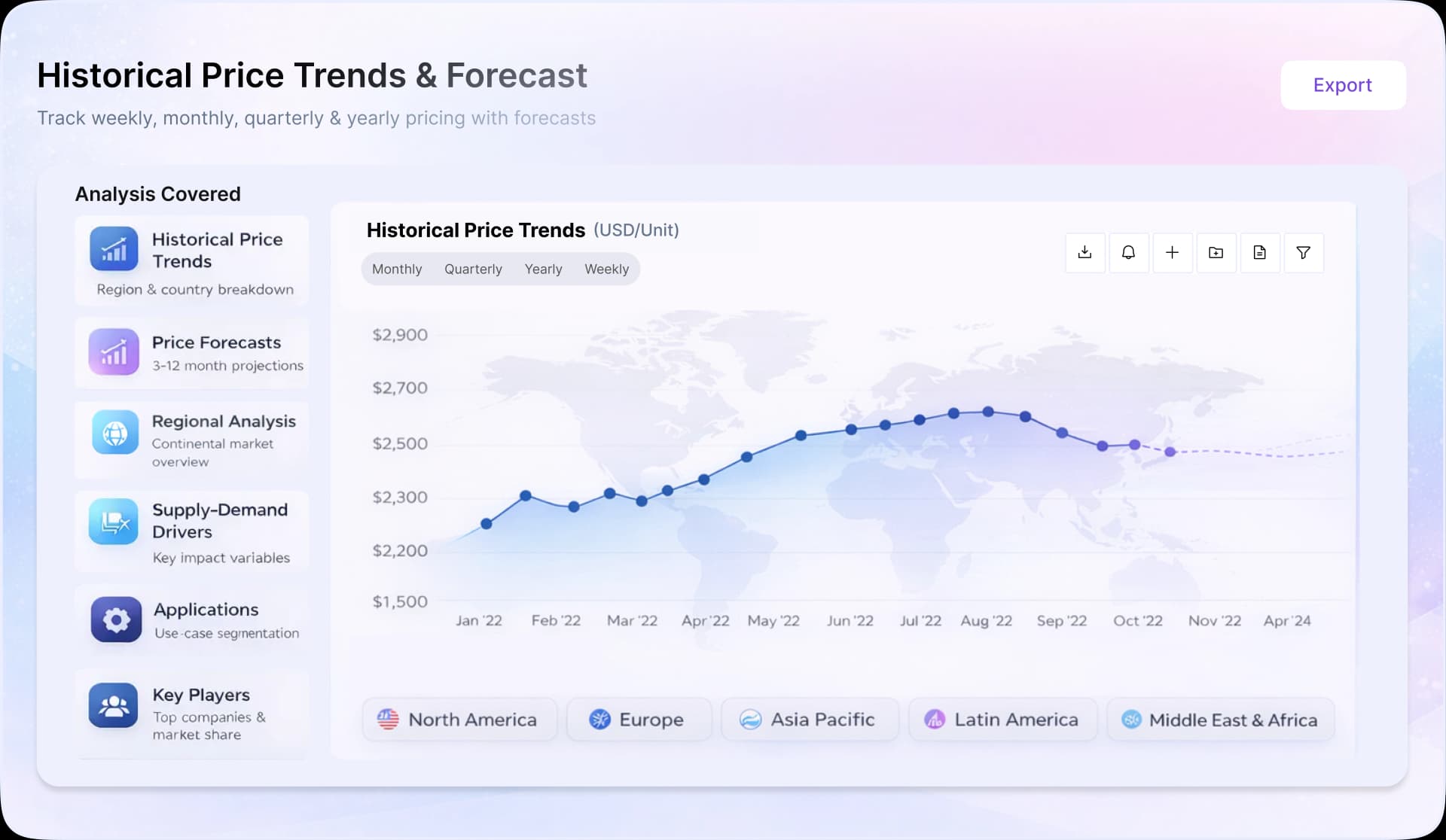

Cocoa prices trended downward, falling over 10% year-on-year at the start of 2026 and extending a broader correction of more than 70% from late-2024 highs, primarily driven by recovering production and improved harvest expectations in key West African origins. Favourable weather conditions in Côte d’Ivoire and Ghana, accounting for over 60% of global supply, supported early crop development, while expectations of surplus in the 2025/26 season weighed further on sentiment.

On the trade side, declining futures did not immediately translate into lower retail prices, as manufacturers continued to process higher-cost inventories purchased earlier, maintaining elevated shelf prices. Consumption patterns reflected pressure, with around 90% of Easter confectionery demand still chocolate-based and total seasonal spending estimated at about $3.3 billion yet supported by reformulation and cost control strategies rather than volume growth. Additionally, regulatory shifts such as traceability requirements increased compliance costs, influencing sourcing decisions.

Analyst Insight

According to Procurement Resource, in the near term, cocoa prices are expected to remain under pressure from surplus expectations, though weather variability and supply-side risks may sustain market volatility.

Related Report

Our Clients

Procurement Resource Database

Turn price intelligence into action with the Procurement Resource Database. Log in or subscribe to unlock live price trends, historical charts, supplier databases, cost curves, and analyst-backed insights across chemicals, agriculture, energy, packaging, and more. Use these tools to benchmark your contracts, plan budgets with confidence, and stay ahead of market moves on every product you buy.

Cocoa Dashboard Inclusions

0

+Products

0

+Regions

0

+Subscriptions

| Product | Category | Region | Price | Last Updated Month |

| Cocoa | Energy, Metals and Minerals | South America | US$ 917/MT | October 2025 |

Stay updated with the latest cocoa prices, historical data, and tailored regional analysis

During Q4’25, cocoa prices gradually eased after the extreme highs seen earlier in 2025. In West Africa, farmers continued selling into the market, but demand from processors remained limited. Many manufacturers had already secured stocks at high prices, so immediate buying slowed. At the same time, the use of cocoa alternatives like shea butter and lab-grown fats reduced pressure on natural cocoa, keeping prices softer.

In North America and Europe, cocoa demand remained weak. Chocolate makers adjusted recipes, replacing some cocoa with cheaper fats, and processing volumes fell to multi-year lows. Slower consumption and cautious purchasing helped keep market prices under control. Manufacturers also focused on cost management and product reformulation, which reduced urgency for large cocoa purchases.

Overall, cocoa prices fell from their record highs but stayed above long-term averages. Farmers received some support from government price guarantees, while manufacturers continued to explore substitutes and optimize production.

In the third quarter of 2025, cocoa prices showed a downward trend after reaching record highs in late 2024 and early 2025. The drop was mainly driven by weaker demand from chocolate manufacturers, who continued to struggle with high production costs and shrinking profit margins.

Cocoa grind data a key indicator of industrial demand showed noticeable declines across major regions, confirming that demand destruction persisted. Europe, Asia, and North America all reported lower grind volumes compared to the same period last year, reflecting softer consumption.

On the supply side, global cocoa availability began to stabilize slightly. Improved weather conditions in parts of West Africa and signs of recovery in mid-crop output in Côte d'Ivoire helped ease earlier supply pressures. Additionally, new plantings in Ecuador started to bear fruit, adding some relief to global supply chains. Still, structural problems like ageing trees in Ghana and Indonesia remained unresolved and limited a strong production rebound.

Ghana’s decision to raise producer prices by over 60% ahead of the next season added upward pressure, especially on competing producers like Côte d'Ivoire. However, the market was largely focused on short-term supply recoveries and sluggish demand, which kept overall sentiment bearish during the quarter.

In the second quarter of 2025, cocoa prices showed significant fluctuations, driven by both market corrections and renewed supply fears. After peaking at historic highs in late 2024, prices had dipped sharply in early 2025 as expectations of improved harvests and reduced demand temporarily eased pressure on the market. However, by May, prices bounced back strongly, rising more than 20% within the month. This sharp recovery was largely due to renewed concerns over cocoa quality and ongoing weather challenges in West Africa, especially in the Ivory Coast and Ghana — the world’s two biggest producers.

Although harvest volumes in some areas were slightly higher than the previous year, much of the crop was of lower quality, prompting chocolate manufacturers to push back on supply. Export delays and drought conditions in key growing regions further strained the supply chain. Meanwhile, producers like Nigeria tried to ramp up exports, helping stabilize the market somewhat. But with buyers wary of inconsistent quality, prices remained highly sensitive.

In the first quarter of 2025, cocoa prices experienced a sharp and steady rise, driven by ongoing climate-related disruptions and deepening global shortages. Severe weather, including flooding and disease outbreaks in key producing countries like Côte d’Ivoire and Ghana, further tightened supply, already under strain from years of underinvestment and poor growing conditions.

The supply shortfall was significant, with global production estimated to have dropped to one of the lowest levels in decades. Meanwhile, demand for chocolate remained strong and relatively unaffected by rising prices, keeping pressure on the market.

Compounding the supply squeeze, newly imposed U.S. tariffs on cocoa and chocolate imports from major producing countries pushed costs higher for American manufacturers. This led to a ripple effect through the supply chain, with both mass-market and specialty chocolate producers facing increased raw material expenses.

Craft chocolate makers, already paying premium prices for quality beans, found themselves caught between soaring costs and shrinking profit margins. Many raised retail prices, reduced product lines, or explored alternative cocoa origins to stay afloat.

In the second half of 2024, cocoa prices remained elevated following a record-breaking surge earlier in the year. Although prices had eased slightly from their April peak, they still hovered well above historical averages. This sustained high level was mainly due to poor harvests in Ghana and Ivory Coast—the world's top cocoa producers—caused by El Niño-related weather extremes and long-standing issues such as aging cocoa trees and plant diseases. Fertilizer shortages and rising input costs also added to the pressure on global supply.

Despite efforts by Ghana’s Cocobod to support farmers through sharp farmgate price hikes, these increases lagged behind the rise in global market prices. The government’s reliance on a forward sales model and international syndicated loans meant that farmers missed out on peak market gains, as prices were locked in months earlier. While the price hikes aimed to deter smuggling and improve farmer incomes, high inflation and logistical costs continued to squeeze profit margins.

Meanwhile, chocolate prices soared in many countries, with consumers paying significantly more for seasonal treats, especially during Christmas. Retailers and manufacturers passed the cost burden to shoppers, citing the steep rise in cocoa costs and other inputs.

During Q2 2024, cocoa prices remained elevated, reflecting ongoing challenges in the global supply chain and the impact of adverse weather conditions. The upward trend in prices, which began in mid-2022, continued into the quarter, driven by persistent supply constraints and rising production costs. Despite a slight correction in May from record highs reached in April, overall market sentiment remained bullish, with prices expected to stay high throughout the year.

The cocoa market faced significant supply disruptions, particularly from West Africa, which accounts for the majority of global production. Adverse weather conditions, notably the lingering effects of El Niño, led to drought stress in key producing regions like Ghana and Côte d’Ivoire, severely impacting cocoa yields. Additionally, labor shortages in the trade and logistics sectors exacerbated supply chain issues, driving up global freight costs and adding further pressure to cocoa prices.

In Ghana, one of the leading cocoa producers, production was notably below expectations due to these adverse conditions, contributing to the global supply shortfall. The country also faced challenges from illegal mining activities, which reduced the land available for cocoa cultivation. Meanwhile, other regions, including Nigeria, experienced significant declines in cocoa exports, further tightening global supply.

The industry also faced rising costs related to input and labor. Fertilizer shortages, driven by disruptions in the global supply chain due to the Russia-Ukraine conflict, increased production costs, affecting the quality and quantity of cocoa beans. Rising labor costs, particularly in Ghana, also contributed to the overall increase in production expenses.

Demand dynamics further supported high cocoa prices. The global market saw a growing appetite for specialty and premium chocolates, with significant innovation in product development driving up the demand for high-quality cocoa beans. This increase in demand, coupled with the constrained supply, created an environment where prices were likely to remain elevated.

Overall, the cocoa market in Q2 2024 was characterized by tight supply conditions, high production costs, and robust demand, all of which contributed to sustaining elevated price levels.

| Product | Category | Region | Price | Last Updated Month |

| Cocoa | Agriculture, Farming and Commodity | West Africa | 4415 USD/MT | January |

| Cocoa | Agriculture, Farming and Commodity | West Africa | 5288 USD/MT | March |

Stay updated with the latest Cocoa prices, historical data, and tailored regional analysis

The global cocoa market was struggling with its most severe supply deficit in over six decades, primarily due to environmental disruptions, diseases, and aging trees in West Africa, which produces around 60% of the world's cocoa. The result of this supply disruption was evident in the 19% surge in global cocoa prices from an average of 4415 USD/MT in January to 5288 USD/MT in March.

The International Cocoa Organization forecasts an 11% drop in global cocoa production for the 2023/24 season, leading to a significant supply-demand mismatch and driving up prices of cocoa. The ICCO's first forecasts for the 2023/24 cocoa year indicate a supply drop to 4.449 million tonnes and a demand reduction to 4.779 million tonnes.

Further, El Niño weather conditions worsened the situation, causing unseasonal heavy rains followed by dry heat, particularly affecting the Ivory Coast and Ghana. Major cocoa-producing countries experienced significant drops in output, with Ghana revising its production estimates to a 14-year low. Additionally, farmers also struggled with reduced yields due to black pod disease, swollen shoot virus, and trees that exceeded their optimal yield potential.

The financial strain on farmers was further compounded by fixed pricing policies that limit their ability to benefit from rising market prices. In response to these market dynamics, commercial buyers started to secure available cocoa, further pressuring the market. Overall, this supply shortfall is causing higher global prices, increased unit costs, and potential disruptions for processors.

About Cocoa

Cocoa, derived from the seeds of the Theobroma cacao tree, is a crucial agricultural commodity primarily used in the production of chocolate. The seeds, known as cocoa beans, undergo a meticulous process of fermentation, drying, roasting, and grinding to produce cocoa mass, cocoa butter, and cocoa powder.

Cocoa butter is valued for its rich, creamy texture and is also widely used in cosmetic products. The powder serves as a key ingredient in various food products due to its rich flavor and antioxidant properties. Native to the Amazon and Orinoco River basins, cocoa plays a significant role in global economies, especially in West Africa, which dominates global production.

Cocoa Product Detail

Cacao, Cocoa bean, Chocolate bean

Chocolate Production, Baking and Confectionery,Beverages, Cosmetics, Pharmaceuticals, Nutraceuticals

Cargill Incorporated, Cocoa Processing Company Limited (CPC), ECOM Agroindustrial Corp. Limited, PRONATEC AG, Blommer Chocolate Company, Tradin Organic Agriculture B.V.

Regional Coverage

Asia Pacific

Europe

North America

Latin America

Africa

CurrencyUS$ (Data can also be provided in local currency)

Supplier Database AvailabilityYes

Customization ScopeThe report can be customized as per the requirements of the customer

Post-Sale Analyst Support360-degree analyst support after report delivery

Note: Our supplier search experts can assist your procurement teams in compiling and validating a list of suppliers indicating they have products, services, and capabilities that meet your company's needs.

Cocoa Production Process

Cocoa is a natural product obtained from cocoa trees (obtained from cocoa bean that serves as its primary feedstock. Cocoa beans are first cleaned and roasted to develop flavor. The beans are then cracked, and shells are removed to obtain cocoa nibs. These nibs are ground into cocoa liquor. Cocoa butter is extracted from the liquor, leaving cocoa powder, both used in chocolate manufacturing.

Our Price Analysis Methodology

Schedule A Demo

Experience how Procurement Resource transforms raw material price data into clear, decision ready intelligence. Optimise your performance with reliable, expert market data and analysis. Schedule your demo today to experience a live walk-through where our experts will showcase interactive price charts, forecasted prices, and insights driving the prices for your key commodities, tailored to your workflows. Contact us now!

Our Team will be happy to assist you

We are just a text away

Still Need Help ?

Other Related Reports

Cocoa Butter Production from Grinding and Pressing Method

This report provides the cost structure of cocoa butter production from the grinding and pressing methods. When the nibs extracted from cocoa beans are grounded, it produces chocolate liquor.

White Chocolate Production from Cocoa Butter

This report provides the cost structure of white chocolate production from cocoa butter. Cocoa butter is separated from the whole cocoa mass to make a press cake of cocoa beans.

Subscription Plans

Unlock full access to Procurement Resource's price databases, interactive charts, and short-term forecasts for thousands of commodities. Elevate your sourcing decisions by comparing prices across regions, downloading historical data, and layering in analyst-backed insights, all with our flexible plans that scale as your portfolio grows.

Still have any Questions

Contact Us

Price Trend Dashboard - What's Included

Price trends across a diverse portfolio of categories amd products, spanning board to niche chemicas

Coverage extendable to grade-specific chemicals based on procurement requirements

Regular price tracking supported by robust historical datasets

News, policy updates, and key market drivers impacting price movements

Short-term and long-term price outlooks and forecasts

Supply–demand dynamics and capacity-driven market analysis

- Unlimited Users

- Historical Monthly Price

- USA, Europe, APAC Covered

- Monthly Forecast

- 12 Months validity

- News & Events

- 50 Products (Refer Next Page For List)

Related News

View All

Why Procurement Database

Assistance from Experts

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Client's Satisfaction

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Assured Collaboration

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Global Insights

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...