Coking Coal Price Trend Analysis 2026: Supply Demand Analysis, Price Drivers, Latest News, Historical Prices & Market Insights

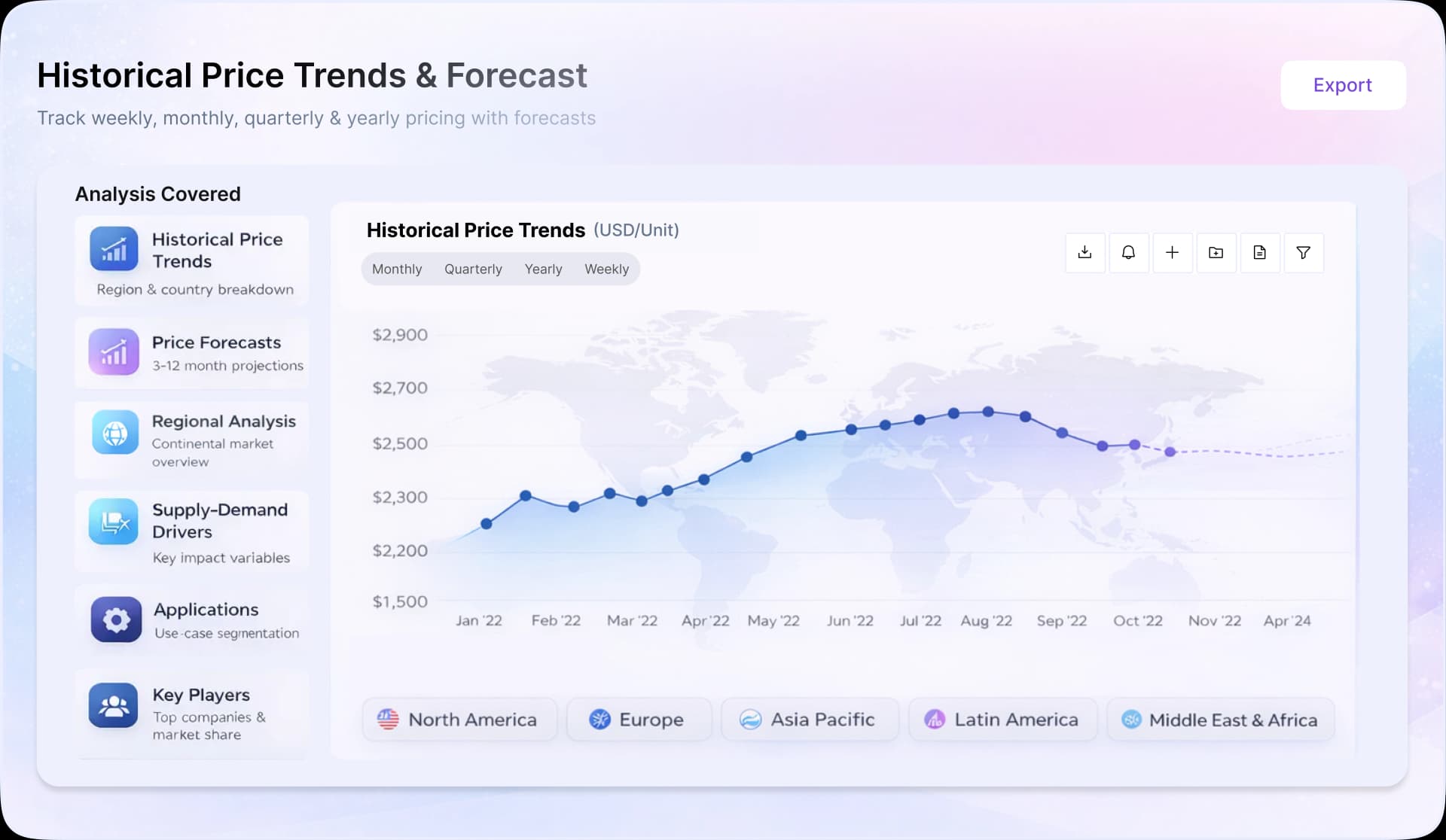

Coking Coal Price Trend Q1 2026

| Product | Region | Incoterm Basis | Price | Last Updated Month |

|---|---|---|---|---|

| Coking Coal | USA | CIF | USD 315.72/MT | April 2026 |

| Coking Coal | India | CIF | USD 365.72/MT | April 2026 |

| Coking Coal | Germany | CIF | USD 354.72/MT | April 2026 |

| Coking Coal | China | FOB | USD 228.72/MT | April 2026 |

| Coking Coal | Canada | CIF | USD 318.72/MT | April 2026 |

| Coking Coal | USA | CIF | USD 315.65/MT | March 2026 |

| Coking Coal | India | CIF | USD 283.65/MT | March 2026 |

| Coking Coal | Germany | CIF | USD 310.65/MT | March 2026 |

| Coking Coal | China | FOB | USD 228.65/MT | March 2026 |

| Coking Coal | Canada | CIF | USD 318.65/MT | March 2026 |

Stay updated with the latest coking coal prices, historical data, and tailored regional analysis

- Global coking coal prices showed a mixed trend in Q1’26, weakening early due to soft steel output and improving later as supply risks and freight concerns increased after geopolitical disruptions.

- Feedstock dynamics remained balanced, with stable coal output but localized supply disruptions tightening availability in parts of Asia.

- Downstream demand remained subdued as global steel production declined, limiting procurement despite late-quarter recovery signals.

Asia

Coking coal prices in Asia followed a weak-to-firm trend in Q1’26, declining early due to sufficient mine supply and cautious steel mill buying, then recovering as supply tightened and freight risks increased. China’s coal mining and washing sector expanded steadily, while imports rose modestly by 1.3% year on year, indicating stable upstream availability and continued reliance on seaborne supply. However, downstream demand remained limited as global steel production fell, with total output at 147.3 million tonnes in January 2026, down 6.5% year-on-year, which reduced coking coal consumption. Late-quarter recovery was supported by safety checks and improved steel output.

Europe

Coking coal prices in Europe remained under pressure in Q1’26 due to weak steel production and reliance on imports. Steel demand stayed soft, with EU output trends reflecting broader global decline, reducing blast furnace activity and coking coal consumption. Import dependence exposed the region to higher freight and energy costs after the Strait of Hormuz disruption, as the route carries about one quarter of global seaborne oil trade, increasing logistics and input cost pressure. Despite this, weak downstream demand limited upward momentum.

North America

Coking coal prices in North America remained relatively stable in Q1’26, supported by export-linked demand but constrained by moderate domestic steel activity. U.S. coal exports reached 23.5 million short tons in Q4’25, indicating strong export positioning entering Q1’26, which supported sentiment. Domestic demand remained limited due to stable steel output and structural shifts toward electric arc furnace production. Indirect cost pressure from higher fuel and freight costs following geopolitical disruption influenced market conditions but did not significantly alter supply.

Analyst Insight

According to Procurement Resource, coking coal prices are expected to remain range-bound, with recovery dependent on steel output improvement and any further supply disruptions affecting seaborne trade.

Our Clients

Procurement Resource Database

Turn price intelligence into action with the Procurement Resource Database. Log in or subscribe to unlock live price trends, historical charts, supplier databases, cost curves, and analyst-backed insights across chemicals, agriculture, energy, packaging, and more. Use these tools to benchmark your contracts, plan budgets with confidence, and stay ahead of market moves on every product you buy.

Coking Coal Dashboard Inclusions

0

+Products

0

+Regions

0

+Subscriptions

Asia

During Q4 2025, coking coal prices in Asia displayed mixed movements rather than a single directional trend, shaped by alternating supply and demand influences. In the early part of the quarter, prices moved upward as tighter safety supervision and environmental checks constrained mine output, keeping spot availability limited and inventories low. Demand from coke producers and steelmakers remained supportive during this phase, encouraged by stable molten iron production and firm coke market conditions. However, this strength was not sustained consistently. As the quarter progressed, import inflows increased, and domestic mine operations gradually resumed, easing supply tightness. At the same time, downstream buyers became more cautious, shifting toward need-based procurement and reducing market activity. This led to intermittent price softening. By the latter part of the quarter, supply conditions appeared more balanced, while demand weakened, resulting in a period of stabilization to slight decline. Overall, the Asian market reflected alternating phases of firmness and easing, leading to a mixed price trend across the quarter.

Europe

Coking coal prices in Europe broadly resembled the trend observed in the Chinese market during Q4 2025. Early in the quarter, prices firmed alongside global supply tightness and supportive sentiment from Asian markets. Steel producers maintained stable operations, lending initial support to demand. As supply availability improved later in the quarter and global market pressure eased, European buyers slowed procurement. Demand from the steel sector softened, leading to weaker trading activity and price pullbacks toward the end of the quarter. The overall pattern mirrored Asia’s transition from firmness to easing, rather than showing a distinct regional trajectory.

North America

North American coking coal prices also followed a pattern similar to the Chinese market during Q4 2025. Prices found early support from steady steel production and export demand, while mine output remained controlled. This phase aligned with global supply tightness seen earlier in the quarter. As international supply conditions improved and export demand weakened, price momentum softened. Steelmakers reduced raw material purchases, and market activity slowed. By the end of the quarter, prices eased from earlier levels, reflecting the same broad rise-and-correction pattern observed in Asia.

Asia

Coking coal markets in Asia experienced fluctuating conditions through the quarter. Supply disruptions at mines, combined with restrictions on certain grades and logistical issues in cross-border shipments, created intermittent periods of tightness. Steelmakers sustained high production rates, keeping procurement interest firm in the early part of the quarter. As the quarter progressed, supply gradually stabilized with more mines resuming operations. Inventories improved, and downstream buyers adjusted to a more cautious stance. While steel production levels stayed elevated, profit margins narrowed, leading to restrained restocking. This created a transition from earlier firmness to a more balanced and eventually softer trend. Overall, Asia displayed notable fluctuations, driven by alternating phases of tightness and weaker procurement sentiment.

Europe

European coking coal activity was steadier compared to Asia. Import supply lines from traditional producers remained intact, ensuring the availability of high-quality blends. Market participants in the region showed conservative procurement strategies, with many mills limiting intake to immediate needs. Steel demand provided limited support, with high energy costs and uneven order books affecting operating rates. Maintenance stoppages at several facilities added to the cautious approach. As a result, trading volumes stayed controlled, and prices held within a narrower range. The regional balance leaned toward stability rather than volatility, reflecting a contrast with Asia’s shifting dynamics.

North America

In North America, supply remained reliable, and producers maintained consistent output levels. Export commitments to overseas buyers were fulfilled, while domestic steelmakers secured sufficient material to cover their requirements. The balance between exports and local consumption supported steady market conditions. Demand from construction and automotive sectors added a layer of stability, though buyers did not pursue large-scale restocking. Instead, procurement was centered on near-term operational needs. Toward the close of the quarter, with overseas markets softening, additional volumes became available domestically, further reinforcing the sense of stability.

| Product | Category | Region | Price | Last Updated Month |

| Coking Coal | Operating Costs, Logistics and Utilities | China | 194 USD/MT | April 2025 |

Stay updated with the latest Coking Coal prices, historical data, and tailored regional analysis

Asia

During the second quarter of 2025, the Asian coking coal market witnessed a drop in prices. The prices were about 194 USD/MT (Spot) during the month of April in the Chinese markets. The quarter commenced on a fairly stable basis, but cautionary sentiment prevailed thanks to a subdued trading environment and limited buying interest from the downstream sectors. Buyers kept themselves largely restricted to bare essentials. During the rest of the quarter, oversupply gained momentum. Coal mine inventories were high, and some sites reduced production. The steel industry moved into a slower cycle, and the expected demand boost from iron production did not occur. Although some downstream markets initially tried to restock, they soon reverted to cautious buying habits. By quarter-end, price declines had narrowed, but market conditions were still soft.

Europe

In Europe, coking coal prices also moved downward, influenced by reduced industrial production and seasonally weaker demand from the steel and building industries. While global tensions nudged wider commodity markets, however, European coking coal markets experienced minimal supply dislocation. Steel mills ran at below capacity due to weak demand and squeezed margins, further reducing their intake of coal. The speculator buying was avoided by the traders, who held minimal inventory and bought only on requirements. The lack of supply chain impediments and ongoing material availability from exporting countries kept the supply chain well-liquidated. Though short-term pricing action paused, the trend overall remained weak since regional demand did not build up during the quarter.

North America

North America's coking coal market also reflected the patterns of other markets, with prices falling influenced by moderate production and cooled industrial activity. Domestic steel mills experienced conflicting signals; some mills temporarily raised output, but others curtailed operations due to muted construction demand and maintenance outages. Export demand provided feeble support, but it was not sufficient to counter the negative drag from domestic excess supply. Mining activities in most cases, continued with regular output, leading to an accumulation of stocks. Purchasers practiced caution, holding back on orders in anticipation of a price fall. Absent a major change in consumption patterns, prices continued to follow a downward trend.

| Product | Category | Region | Price | Last Updated Month |

| Coking Coal | Operating Costs, Logistics and Utilities | China | 214 USD/MT | January 2025 |

| Coking Coal | Operating Costs, Logistics and Utilities | China | 196 USD/MT | March 2025 |

Stay updated with the latest Coking Coal prices, historical data, and tailored regional analysis

Asia

During the first quarter of 2025, Asia's coking coal market exhibited a fluctuating trend, influenced by regulatory changes, weather disruptions, and shifting demand. Prices were approximately 214 USD/MT (CIF) in January and declined to around 196 USD/MT by March in the Chinese market. At the beginning of the quarter, supply from major producing nations was affected by excessive rainfall, restricting mining activity and increasing production costs. Additionally, new regulations requiring coal exporters to retain a portion of foreign exchange earnings domestically resulted in tighter cash flows and operational adjustments. These factors initially supported prices, particularly for lower-grade coal, which witnessed firm demand from Indian and Southeast Asian buyers. However, as supply conditions gradually improved and competition intensified, especially from South African exporters, prices came under pressure. Chinese demand remained steady but selective, focused on power generation and stainless-steel production. Toward the end of the quarter, weaker export demand and cautious trading sentiment introduced a bearish tone, although domestic consumption in countries such as Indonesia provided some stability.

Europe

In Europe, the coking coal market remained generally weak throughout the quarter, influenced by subdued industrial activity, strong renewable energy generation, and low electricity consumption. Although some coal-fired power plants in countries such as Germany and Poland resumed operations due to temporary increases in gas prices, the resulting rise in coal usage was short-lived. Broader market dynamics continued to reflect the region’s focus on decarbonization, with stringent environmental regulations and increased investment in renewable energy limiting coal consumption. Demand from key sectors, including construction and steel, remained subdued, while importers adopted a cautious procurement approach, relying largely on long-term contracts. Overall, reduced consumption and limited industrial support kept coking coal prices under pressure during the quarter.

North America

In North America, the coking coal market maintained a relatively stable pricing trend, supported by steady industrial demand and localized supply constraints. At the beginning of the quarter, a cold weather spell disrupted mining operations, creating short-term supply tightness and supporting prices. Steel sector demand remained firm, aided by trade policies that encouraged domestic production. Despite lower coal consumption in the power sector, the metallurgical segment sustained overall demand. As weather conditions improved, supply normalized, while purchasing activity remained cautious amid regulatory uncertainty under the incoming U.S. administration. Overall, prices remained stable, supported by consistent demand from key industrial sectors.

Asia

In Asia, the coking coal market demonstrated mixed trends. While Australian premium coking coal prices held steady through most of the period, Chinese demand remained subdued due to ongoing challenges in their real estate sector and steel industry.

Indian buyers emerged as a crucial market force, helping offset the weakness in Chinese demand. Their increased steel production capacity and consistent buying patterns provided important support to regional prices. Mongolia's growing role as a supplier introduced new dynamics to the Asian market, particularly as they ramped up their transportation infrastructure.

Europe

The European market faced unique challenges during this period. Polish producer JSW's reduced output in the second quarter set the tone for the latter half of the year, with production and sales volumes remaining constrained. This tightness in European supply was partially offset by increased imports from various sources, including North America and Australia. The region's steel producers maintained cautious buying patterns, carefully managing their inventory levels in response to uncertain economic conditions.

North America

North American suppliers experienced a challenging period, particularly in the latter months of the year. US producers faced pressure from competitive Australian prices in key export markets, leading some to reduce production. The announcement of Chinese import duties on US coal for early 2025 prompted suppliers to actively seek alternative markets, particularly in India. Despite these challenges, North American premium grades maintained their market presence, especially in regions where quality specifications were paramount.

| Product | Category | Region | Price | Last Updated Month |

| Coking Coal | Operating Costs, Logistics and Utilities | China | 339 USD/MT | January’24 |

| Coking Coal | Operating Costs, Logistics and Utilities | China | 284 USD/MT | June’24 |

Stay updated with the latest Coking Coal prices, historical data, and tailored regional analysis

Asia

Coking coal prices in China fell in the first half of 2024 due to weak demand from the property and infrastructure sectors (which are major consumers of steel) and steel mills in the absence of any significant government stimulus policies. An oversupply in the market, driven by increased exports from Australia, particularly after the rainy season in Queensland and a sharp rise in spot cargoes from a major Australian coal producer, further pressured prices.

The monthly average prices in the Chinese coking coal market went from about 339 USD/MT in January’24 to around 284 USD/MT in June’24. Overall, the combination of weak demand, oversupply, and temporary market rebounds without substantial changes in market fundamentals led to a decline in coking coal prices in China in the first half of 2024.

Europe

The coking coal market in Europe was not any different than the Asian market during the said period. The prices were found to be declining in most of the European markets as well. Given Europe’s position as a significant importer of coking coal, the domestic market was affected by the declining prices in Australia due to oversupply and decreased demand in Asia, potentially leading to price reductions and market adjustments in Europe.

North America

In the first half of 2024, the North American coal market experienced wavering trends driven by a combination of global and domestic factors. Coking coal prices in North America were influenced by broader global market dynamics, including weak demand from key steel-consuming countries like China and India, which led to a decline in global coking coal prices. The oversupply situation in the Australian market, coupled with subdued demand in Asia, put additional downward pressure on prices, indirectly affecting North American producers.

The shutdown of the Donkin coal mine in Canada due to safety issues added to regional supply constraints, though the mine was later permitted to resume production. Meanwhile, Sunrise Coal, a significant U.S. producer, announced layoffs amid declining demand and market uncertainty. Overall, the North American coal market in H1 2024 reflected the broader global oversupply and weak demand trends, leading to challenging conditions for both coking and thermal coal producers.

| Product | Category | Region | Price | Last Updated Month |

| Coking Coal | Operating Costs, Logistics and Utilities | Asia | 253.18 USD/MT | July’23 |

| Coking Coal | Operating Costs, Logistics and Utilities | Asia | 332.14 USD/MT | December’23 |

Stay updated with the latest Coking Coal prices, historical data, and tailored regional analysis

Asia

In Asian countries, the coking coal prices inclined from an average of 253.18 USD/MT (Spot FD) in July’23 to 332.14 USD/MT in December’23. The market rose on the back of the rising scarcity of the product.

The market tensions further intensified due to the exponential demand for the commodity amid limited supply. The coal operators, however, were distressed by adverse weather conditions and disruptions caused by the unseasonal rainfall and floods. Additionally, the unpredictability of the production rates further caused an upset in the supply-demand equilibria, leading to an incline in the coking coal price trend.

Europe

During the third and fourth quarters of 2023, the coking coal price trend inclined owing to high downstream demand for electricity and heightened international procurement rates. However, the commodity supply was slow, widening the gap between the demand and supply sectors.

Another disparity came from logistical challenges and adverse weather conditions which supported the rise in the coking coal price trend. However, the growth rates of the prices slowed down in the fourth quarter as the downstream industries started utilizing natural and renewable sources of energy to reduce their dependency on coking coal and its derivatives.

North America

Primarily driven by the demand from the downstream industries and the rise in export rates, the North American coking coal market enjoyed an upward trend in its prices. However, this inclination in the market dynamics was short-lived and by the end of the third quarter, the price trend began its southwards trajectory.

The shifting sentiments of the consumers and the province of renewable sources of energy, along with the advent of government initiatives favoring the alternatives of traditional sources, caused a significant reduction in the procurement rates of coking coal and thus resulted in the decline in the coking coal price trend.

Asia

Coking Coal is mined from the earth and is used in very energy-intensive processes like making fuel, coal, electricity, steel, cement, etc. The first half of the year 2023 witnessed a downturn in Coking Coal prices. Since both India and China had access to cheaper Russian oil, the oil was consumed more than coke, and the demands from the downstream sectors took a plunge. Since the markets were still struggling to revive after the lockdown was lifted, the Chinese manufacturing sector could not touch the pre-lockdown levels. Several other geopolitical tensions also had their part to play.

The average spot prices stood at around 360 USD/MT in the Chinese domestic market in Jan’23, which were reduced to about 240 USD/MT in June’23, registering an approximate depreciation of about 33%. Overall, feeble market sentiments were observed.

Europe

The European market witnessed a fluctuating price pattern for Coking Coal during H1’23. As the Russian supplies were heavily sanctioned, the imports rose from the Middle East and the USA. Due to high inflation, the downstream industries struggled to maintain production, and with halts in operation, the demand for Coking Coal saw a sharp decline in the region. After wavering a little in the first quarter, the Coking Coal prices tumbled in the second. Overall, bearish market sentiments were observed.

North America

The American Coking Coal market almost replicated the European market as inflation hit high in the US as well, two major US banks collapsed, and the interest rates flung high. So, with very limited demands from the consuming sectors, the prices declined throughout the discussed time period.

Asia

The coking coal prices exhibited diverse trend in the Asia-Pacific region. In China, the coking coal prices kept high in July and fell drastically considering the weak demand and cautious buying activity in the market. With the government announcing a ‘property guarantee policy’ anticipating a recovery in real estate, the demand from the steel and construction sector rebounded. Thus, the coking coal price trend stabilized in mid-August. The prices consolidated, however the willingness to purchase was still general.

In India, where most of the coking coal is largely imported the prices touched new highs in the third quarter. These high continued till the next quarter with little relief to the steel manufacturers. In Australia, the coking coal prices inclined as La Nina caused many problems with the Australian thermal coal supply and exports, thus causing shortages worldwide.

The price trend for coking coal stabilized in the fourth quarter as the supply chains stabilized. The high prices were being driven by temporary supply disruptions and with the trade normalisation along with higher production the prices fell. However, the prices were still higher than in the past years.

Europe

The current economic backlash owing to the continuing Russia-Ukraine conflict triggered an acute energy crisis in Europe. The prices of crude oil, gas and related products rose drastically giving way to double-digit inflation. The high prices of coking coal prices were due to the higher seasonal demand. However, the prices stabilized in the fourth quarter as Australia replaced Russia as the major exporter of Coking Coal to Europe. Because of high inflation low activities of downstream steel mills were observed, which pulled down the demands and caused the market prices to fall.

North America

The high electricity prices and diminishing availability of coking coal due to lower exports from Australia have led to refineries decreasing production. The short supply amid high demand caused the coking coal prices to inflate throughout the North American market. The supply chains normalised in the fourth quarter causing the price trend to stabilize with a series of occasional inclines and declines.

Asia

To accommodate the ever-increasing demands of its power sector, India relies heavily upon imports. Amid the ongoing geopolitical dynamics and weather disturbances, the price trend of coking coal exploded globally. The prices rose 3-fold to around 450 USD/MT compared to the year back at 120-130 USD/MT. Coking coal is one of the primary feedstocks required for steel production.

Hence, due to the rising costs of inputs, the margins of the Indian steel industry are affected. According to ISA (Indian Steel Association), the price of coking coal in steel production is around 28,000-30,000 INR/MT, which accounts for 40-45% of the entire production cost, provided all the other variables are kept constant.

In April, the Chinese imports of coking coal from Russia reached a record high due to the discounted prices offered by Russia before the European embargo. Coking coal prices went from 3151.3 RMB/ton in April to 2811.4 RMB/ton in June 2022. This price decrease was due to the decreased demands from the downstream sectors. Though the Chinese market for coking coal weakened towards the end of this quarter, the prices are still higher than the previous year.

Europe

During this quarter, coking coal prices remained gusty due to the robust and persistent demand from the European states despite the constant supply chain disruptions. Many EU member states depend on Russia to fulfil its coal requirements, and the current sanctions triggered an acute energy crisis in Europe. The coal prices averaged 374 USD/MT in the forecast period.

North America

For this quarter, the price trend in the United States remained strong. Per ton price of coking averaged around 333-370 USD.

Asia

Average coking coal prices were around 2,665 RMB/MT, up 72.86% over the same period last year. On January 20, the commodities index for northern coking coal was steady from the previous day at 196.68, down 29.31% from the cycle high of 278.23 on November 9, 2021, and up 337.94% from the cycle low of 44.91 on January 28, 2016.

In terms of downstream coke, the price of coke in Shanxi was 2,938 RMB/MT the previous weekend. The coke market price remained constant for a time. Russian exports accounted for around 10% of the world's met coal trade in terms of volume. Customers from China and India had been purchasing spot Russian material at a discount to Australian pricing.

Separately, the export window for Chinese coals increasingly opened up as a result of the international market upswing. At the end of March, worldwide coking coal prices for premium hard grades were 150 USD/MT higher than domestic Chinese pricing, enabling for significantly more competitive exports of Chinese materials.

Europe

European thermal coal quotes went fresh historic highs with restricted supply on the global market and Russia’s ongoing military campaign in Ukraine. Russian coal exports fell since the start of the crisis in Ukraine. Shipping records revealed that coal continued to be delivered from Russian ports to Europe, but several big energy corporations, including Centrica, Vattenfall, Orsted, and BP, chose to wait-and-see to buy Russian coal, fearing future penalties.

In reality, global coal markets were the target of an experiment on the hypothetical removal of 1/6 of the supply, accounting for the part of Russian coal in the world market, that led to an unprecedented spike in prices. As of March 09, 2022, the indices rose above 415 USD/MT, eventually correcting to 360 USD/MT.

North America

Coking coal prices in the United States were 388 USD/MT during the month of March.

Asia

Heavy rains were observed in the Shanxi region of China, the nation's main coal producing province, after record floods slammed the mining district of Henan in July. The floods also hindered China's initiatives to raise fuel supplies to address its increasing energy crisis.

Shanxi Province, which supplied about a third of China's coal supplies in the year 2021, had to temporarily stop dozens of mines owing to flooding. Although several sites progressively restored functioning afterwards. While safety difficulties and flooding hampered domestic mines in China, border barriers between Mongolia and China and ongoing diplomatic disputes between China and Australia only aggravated the situation.

Hard coking coal prices resumed a surge that started in October 2020, reaching record levels of 600 USD/MT CFR China, before falling dramatically in November and stabilising at rates of around 400 USD/MT CFR China.

While coal imports declined by 26.8% year on year, monthly imports increased by 6%, continuing the rising trend from 14.85 MT in October 2021 in India. Meanwhile, the country's coal imports fell by 22.5% in November 2021 to 15.78 MT, down from 20.35 MT in the same month last year.

On a month-to-month basis, coal imports grew marginally by 0.21% in November 2021, to 15.75 MT. India's import demand was muted following the conclusion of the festive season and the improvement of domestic supplies. As a result, the impact of the easing of seaborne prices on import volumes was minimal.

Europe

According to several industry participants, steel manufacturing costs climbed by more than 100 EUR/MT in the last few months of 2021. Mills were projected to increase offer levels further in the coming months, despite no hint of a decline in energy costs across Europe. Because steel demand remained sluggish, mills struggled to sell coking coal at increased prices that fully covered the increased energy expenses.

North America

In November, supply disruptions weighed on US and Canadian coking coal exports, although exceptionally high prices through October and early November encouraged mining businesses to transport cargoes wherever possible. Exports increased in the second half of the year, as mining firms increased output wherever possible in response to the increase demand from Chinese consumers. Nonetheless, output growth had been restricted by the ongoing Warrior Met Coal strike, as well as a generalized labour shortage and substandard rail performance. In October, Argus' daily FOB Hampton Roads estimate reached a record 495.06 USD/MT, up from 112.75 USD/MT a year earlier.

Latin America

Rising demand from China impacted US exports to Brazil. Exports decreased by 21% to 4.54 million tonnes in the fourth quarter of 2021. In August, US and Canadian coking coal exports to China and India increased, while LATAM purchasers sought cheaper Australian cargoes. US exports to Brazil declined 32.7% year on year and 10.8% month on month to 306,199 MT, as customers selected cheaper Australian cargoes. Labor shortages were also a short- and long-term constraint on the US supply.

Asia

Steel demand was mostly bullish in the market outlook, owing to anticipation of a seasonal boost in demand and increasing Covid-19 vaccines. China's supply was limited as a result of local production restrictions tied in part to the country's emissions reduction ambitions.

Coking coal prices increased as freight crisscrossed the globe, with India and Europe purchasing from Australia and China purchasing from the Americas. This has resulted in an increase in voyage times. Stagnant unloading routines at Chinese port resulted in vessel scarcity and raised costs in recent months. In the first half of 2021, ex-China spot demands for seaborne coking coal surged by around 280% year on year.

Europe

Steel mills throughout the world, from China to India, Europe, and Brazil, were trying to secure metallurgical coal amid an unprecedented rise fueled by limited global supplies and disruptions in trade flows caused by the COVID-19 outbreak. Despite the scarcity of supply, spot shipments attracted increased buying interest in Sep 2021 from conventional foreign markets.

North America

The significant rise in seaborne metallurgical coal price that began in mid-second quarter lasted far into the second half of the year, as the global supply-demand balance tightened and a trade tension between Australia and China erupted.

Latin America

The impact of regional COVID-19 lockdowns, which resulted in steel output restrictions, and China's expiration of import quotas earlier in the year put a lot of pressure on the marketplace until late August, as Vale, a major Brazilian miner, noted. Coking coal prices then increased further, reaching 139 USD/MT by the end of September 2021. Numerous nations in LATAM began relaxing lockout restrictions, increasing the demand as steel output steadily increased.

Asia

Spot coking coal prices increased in the first quarter of 2020. This happened because the epidemic limited China's coal production, and Mongolia's decision to close its border with China increased China's imports. Due to the collapse of global steel production outside of China as a result of pandemic confinement, the cost plummeted to approximately 110 USD/MT in April 2020.

Coking coal prices surged at the end of the third quarter as demand from steelmakers beyond the Chinese borders increased production. Intense rainfall in Queensland also encouraged higher prices, but Australian coal's troubles at Chinese customs drove prices down.

Europe

Mining costs grew as a result of heightened safety and social distancing measures in response to the epidemic, while coal prices stayed low. Among other considerations, this resulted in a major proportion of the world's coal mines being unable to stay profitable in 2020, with coking coal having superior economics over thermal coal. By the end of June, Europe constituted about 18% of Australia's spot export volume across a range of grades, comprising premium hard CC, hard CC, pulverised coal injection (PCI), and semi soft coal, up from 5% in 2020. Jastrzbska Spólka Wglowa (JSW), the largest European producer of the product, declared force majeure. Coking coal prices remained low in the second quarter, but stayed stable compared to the first, as the COVID-19 outbreak halted mining operations in Poland.

North America

Reduced fuel prices reduced operational expenses in the coal mining industry, particularly for operators of opencast mines that are dependent on diesel trucks and other equipment.

Low fuel costs benefited countries with a heavy reliance on opencast mining in particular. While average fuel expenses decreased in 2019 as a consequence of reduced diesel prices, these impacts were exacerbated in 2020 as a result of the pandemic and the following significant collapse in diesel prices, leading to additional drops in overall fuel costs.

Reduced total fuel costs translated into a lower share of overall mining supply costs in the majority of countries. After prices stabilised in early 2020, Covid-related demand curtailment pushed coking coal prices lower. Additionally, strikes in the US harmed trade.

Latin America

In 2020, as a result of the global economic crisis caused by the Covid-19 epidemic, the leading coal exporting countries' currencies fell against the USD. South America's emerging markets had been particularly hard hit. In the instance of Colombia, this was primarily owing to the country's reliance on the price of oil.

For the third quarter, spot demand in the Atlantic was primarily limited to Brazilian mills, and despite stronger stockpiles at mines, certain suppliers were still willing to discount. Latin America's raw steel production increased by 8% in May compared to April, primarily due to Brazil, where consumption and production increased from a low starting in April.

About Coking Coal

Coking Coal is a grade of coal which is utilised to make good-quality coke. Coke is an essential fuel as well as a reactant in the blast furnace process for steelmaking. Primary steelmaking companies often have a division which produces coal for coking, particularly to ensure a stable and low-cost production of steel.

Coking Coal Product Detail

Coke production, Reactant, Steelmaking, Liquid fuel, Electricity, Cement manufacturing

Metallurgical Coal

OJSC Raspadskaya Coal Company, Goonyella Riverside Mine (BHP Mitsubishi Alliance), Saraji Coal Mine (BHP Billiton/Mitsubishi Alliance), Mitsui Coal Holdings Pty Ltd., Anglo American plc, Mechel Group, Mitsubishi Chemical Corporation

Regional Coverage

Asia Pacific

Europe

North America

Latin America

Africa

CurrencyUS$ (Data can also be provided in local currency)

Supplier Database AvailabilityYes

Customization ScopeThe report can be customized as per the requirements of the customer

Post-Sale Analyst Support360-degree analyst support after report delivery

Note: Our supplier search experts can assist your procurement teams in compiling and validating a list of suppliers indicating they have products, services, and capabilities that meet your company's needs.

Coking Coal Production Process

- Production of Coking Coal via Mining

Just like other grades of coal, Coking Coal is also derived by mining. It undergoes industrial processing before its utilisation.

Our Price Analysis Methodology

Schedule A Demo

Experience how Procurement Resource transforms raw material price data into clear, decision ready intelligence. Optimise your performance with reliable, expert market data and analysis. Schedule your demo today to experience a live walk-through where our experts will showcase interactive price charts, forecasted prices, and insights driving the prices for your key commodities, tailored to your workflows. Contact us now!

Our Team will be happy to assist you

We are just a text away

Still Need Help ?

Other Related Reports

Coal Liquefication Production from Indirect Liquefaction

This report provides the cost structure of coal liquefication by the indirect liquefaction process. In this process, coal is converted into synthesis gas or syngas, a mixture of CO and H2 gas.

Coal Liquefication Production from Direct Liquefaction

This report provides the cost structure of coal liquefication by direct liquefaction. In this process, coal is exposed to hydrogen at 450°C along with high pressure for one hour in the presence of recycled solvent and iron-based catalyst.

Subscription Plans

Unlock full access to Procurement Resource's price databases, interactive charts, and short-term forecasts for thousands of commodities. Elevate your sourcing decisions by comparing prices across regions, downloading historical data, and layering in analyst-backed insights, all with our flexible plans that scale as your portfolio grows.

Still have any Questions

Contact Us

Price Trend Dashboard - What's Included

Price trends across a diverse portfolio of categories amd products, spanning board to niche chemicas

Coverage extendable to grade-specific chemicals based on procurement requirements

Regular price tracking supported by robust historical datasets

News, policy updates, and key market drivers impacting price movements

Short-term and long-term price outlooks and forecasts

Supply–demand dynamics and capacity-driven market analysis

- Unlimited Users

- Historical Monthly Price

- USA, Europe, APAC Covered

- Monthly Forecast

- 12 Months validity

- News & Events

- 50 Products (Refer Next Page For List)

Related News

View All

.webp&w=1080&q=75)

Why Procurement Database

Assistance from Experts

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Client's Satisfaction

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Assured Collaboration

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...

Global Insights

Throughout 2024, the Asian acetoin market experienced fluctuating trends with regional variations. Q1 began with moderate price increases driven by supply constraints from Chang Chun Plastics' maintenance shutdown in Taiwan. Post-S...